ESG Insights

ESRS Deep Dive on 25 companies from the Netherlands (FY24)

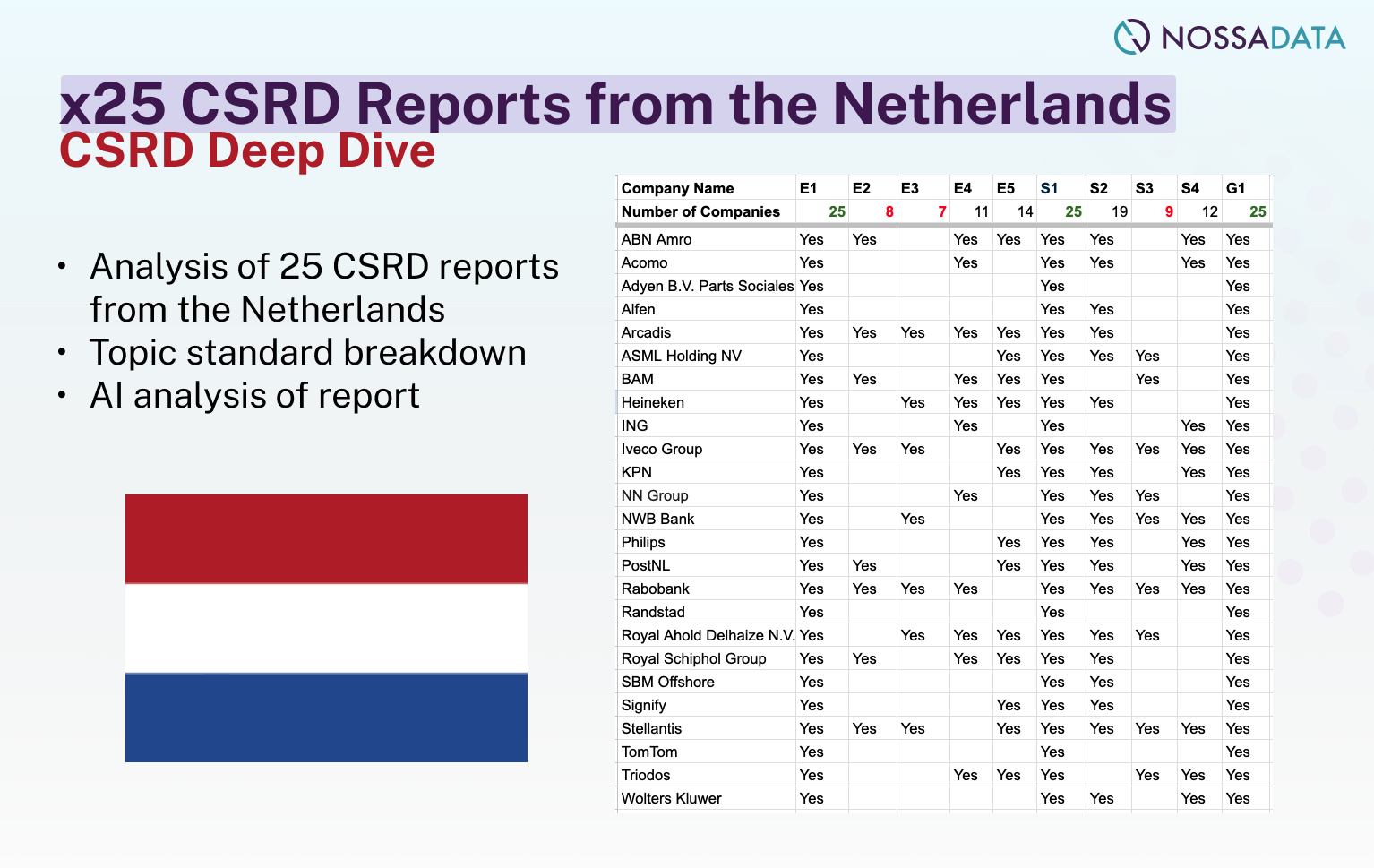

A detailed analysis of 25 Dutch CSRD reports from FY 24.

In June 2023,(ISSB) introduced its inaugural standards, IFRS S1 and IFRS S2, marking a significant step towards global comparability in sustainability-related financial disclosures. To support companies in implementing these standards, the ISSB has recently published an educational guide titled Applying IFRS S1 when reporting only climate-related disclosures in accordance with IFRS S2. This guide is particularly relevant for companies focusing on climate-related risks and opportunities in their first year of applying ISSB standards.

What is the purpose of the guide?

The primary objective of this educational material is to help companies understand which requirements in IFRS S1 are applicable when they disclose only climate-related risks and opportunities in accordance with IFRS S2. The guide reflects the ISSB's intended approach to disclosing climate-related information, which is permitted under the "climate-first" approach.

What is the climate-first approach?

Recognising the challenges companies face in terms of data availability and readiness, the ISSB has provided transition reliefs in IFRS S1 and IFRS S2. This allows companies, in their first year of applying ISSB standards, to focus solely on climate-related risks and opportunities. This is known as the "climate-first" approach.

Under this approach, companies are required to apply IFRS S1 only to the extent as it relates to climate-related disclosures, while fully applying IFRS S2 for climate-related reporting. This temporary relief gives companies time to prepare for broader sustainability reporting in subsequent years.

Key takeaways from the guide

The ISSB's educational guide is a valuable resource for companies navigating the complexities of climate-related financial disclosures. By providing clarity on the applicable requirements of IFRS S1 and IFRS S2, the guide helps companies ensure that their climate-related disclosures are both compliant and useful to investors and other stakeholders.