ESG Insights

ESRS Deep Dive on 25 companies from the Netherlands (FY24)

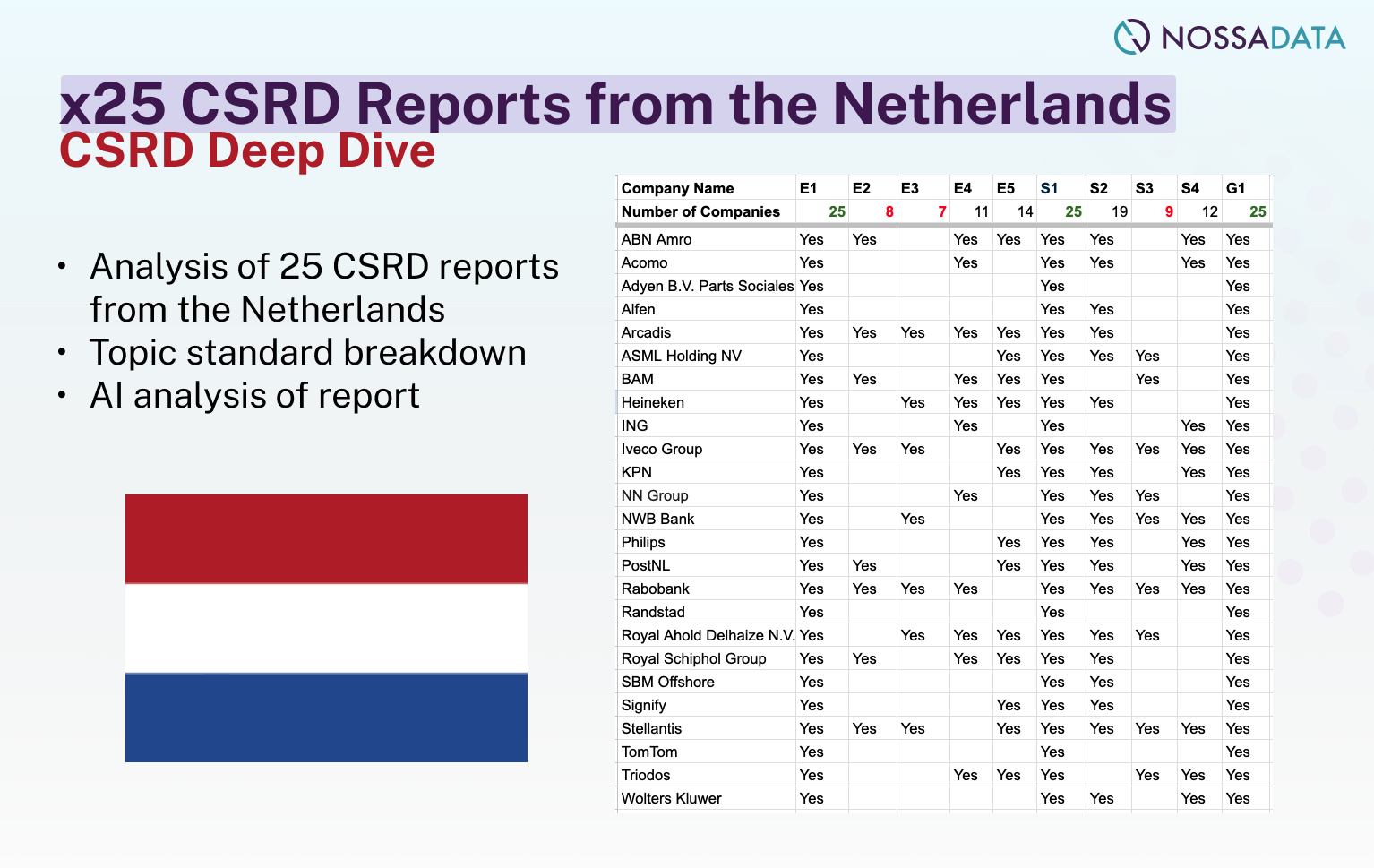

A detailed analysis of 25 Dutch CSRD reports from FY 24.

The EU Omnibus Regulation, often referred to when asking what is the EU Omnibus, is a new way to make sustainability reporting easier across the EU. It brings together different rules to reduce paperwork and increase transparency for companies. This is a big step towards a more unified and efficient corporate sustainability in Europe.

The EU Omnibus Regulation is a big step towards harmonising sustainability reporting requirements across the European Union. This regulation simplifies and unifies various directives to create a more coherent and efficient legal framework for corporate sustainability. The Omnibus Regulation consolidates existing obligations to enhance corporate sustainability across EU member states.

One of the main benefits of the EU Omnibus Regulation is the reduction of administrative burdens on companies. Around 80% of businesses will no longer have to report under the new regulation, which will free up resources for companies to focus on implementing sustainable practices rather than just reporting them.

The ultimate goal of the EU Omnibus is to create a single legal framework that increases transparency and accountability and reduces duplication and inefficiencies. This supports corporate sustainability and economic growth within the European Union.

At the heart of the EU Omnibus Regulation is the consolidation of several key directives into one framework. The Omnibus proposal combines the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD) and the EU Taxonomy Regulation. This simplifies compliance for businesses while ensuring sustainability goals are met.The consolidation simplifies the reporting requirements for companies, provides a clearer path to compliance. Combining these directives the Omnibus Regulation creates a more efficient system, reduces complexity and increases clarity. This benefits businesses and the European Union’s broader sustainability goals.

At the heart of the Omnibus package are the changes to the CSRD, CSDDD and EU Taxonomy. These changes will align the directives with the reality of corporate sustainability, making it easier for companies to comply while contributing to the EU’s environmental and social goals. This holistic approach means the regulation addresses the full spectrum of sustainability issues, from reporting and due diligence to classification and accountability.

The Corporate Sustainability Reporting Directive (CSRD) is one of the cornerstones of the EU Omnibus Regulation. Major changes to the CSRD will change the landscape of corporate sustainability reporting. One of the biggest changes is the reduction of around 50,000 companies to 7,000 that need to comply with the CSRD.

The changes to the CSRD also introduce new thresholds for companies to fall under the scope. Companies now need to meet higher criteria to be within the directive: more than 1,000 employees, more than €50 million turnover or more than €25 million balance sheet total.

The CSRD will be phased in, the first wave covering large public interest entities with more than 1,000 employees will still report for the financial year 2024. See our previous Nossa Data blog posts on CSRD disclosures on the market. However, a 2-year delay is being proposed for the subsequent second wave for all other large undertakings, reporting for the financial year 2027, and the third wave for SMEs with securities listed on EU-regulated markets, who will report for the financial year 2028.

In addition to these changes the CSRD requires the use of European Sustainability Reporting Standards (ESRS) for reporting sustainability performance. This will standardise reporting across the EU and improve the quality and comparability of sustainability disclosures. Nossa Data's AI has come in handy to analyse how ESG disclosures have already changed in light of CSRD, an example summarised here.

The CSRD also aligns with other legislative initiatives, such as the Sustainable Finance Disclosure Regulation (SFDR) and the Corporate Sustainability Due Diligence Directive (CSDDD or CS3D) to create a more integrated regulatory framework.

The Corporate Sustainability Due Diligence Directive (CSDDD) undergoes significant changes under the Omnibus Regulation to reduce complexity while keeping corporate accountability strong. One of the biggest changes is the reduction of due diligence assessments from annual to every 5 years. This reduces the oversight frequency and eases the compliance burden on companies.

Another major change is the restriction of due diligence to direct suppliers only, which simplifies the process but may miss potential abuses further down the supply chain. This focused approach makes due diligence more manageable for companies while still addressing key sustainability issues.

The proposed amendments remove the obligation to terminate a business relationship as a last resort. Instead companies can now opt for suspension, giving them more flexibility in managing their business relationships. But removing the civil liability provisions may undermine accountability as companies may face no consequences for not meeting their due diligence obligations.

The EU Taxonomy aims to provide a common classification system for sustainable finance, to eliminate greenwashing and increase transparency. Under the Omnibus Regulation the EU Taxonomy undergoes major simplification to make it more practical and effective. This includes revising the European Sustainability Reporting Standards (ESRS) to simplify reporting requirements.

To qualify as sustainable under the EU Taxonomy an activity must contribute to one of six environmental objectives without causing significant harm to others. The Do No Significant Harm (DNSH) criteria are simplified making it easier for companies to comply with the classification system. These changes will make the EU Taxonomy more user-friendly and promote its widespread adoption across the EU.

The Omnibus Regulation focusses on large companies given their significant environmental impact. They will need to navigate new compliance requirements which prioritise increased accountability and transparency in their sustainability practices. The regulation’s focus on large entities aligns with the EU’s broader goal of driving substantial progress in corporate sustainability.

But the Omnibus Regulation may face political opposition from groups that resist corporate sustainability measures. This may complicate the implementation process and will pose challenges for large companies as they need to comply with the new requirements.

Despite these hurdles the regulation makes corporate accountability and the role of large companies in achieving sustainability goals clear.

SMEs although not the main focus of the Omnibus Regulation are still impacted. Although they do not have mandatory ESG reporting requirements, stakeholders like investors and customers are imposing these requirements on them. As sustainability reporting becomes more mainstream SMEs will face various ESG information requests from different stakeholders and will complicate their reporting process.

To address these potential burdens the Omnibus Regulation introduces the ‘SME shield’ which limits information requests from large companies to their SME direct business partners. This provision reduces the compliance costs and simplifies the reporting process for SMEs and makes it easier for them to manage their sustainability obligations. The regulation also promotes gradual adoption and eases the learning curve for smaller companies.

The simplification of the compliance process will benefit SMEs the most, reducing excessive sustainability reporting requests and protecting them from burdensome information demands from larger entities. This way SMEs can contribute to sustainability goals without being overwhelmed by the complexity of reporting requirements.

National laws play a key role in the implementation of the Omnibus Regulation. The regulation allows EU member states to set their own civil liability conditions, so companies address sustainability-related harm within the frameworks of their respective national law systems. This eliminates the EU-wide civil liability regime and companies will be under the applicable liability regimes of the member states.

Oversight of compliance will be managed by national authorities in the member states, with penalties for non-compliance. While this decentralization gives flexibility, it also creates uncertainty about how the existing national laws on sustainability will interact with the new regulation. A consistent approach across the EU is crucial for the regulation’s success.

The implementation of the Omnibus Regulation will be phased, companies will have time to adjust. The first group of companies has to comply by mid-2029. The first wave of entities has to comply with the CSRD for the financial year ending 31 December 2024, followed by subsequent waves in the following years.

Significant delays are proposed for the implementation of the Corporate Sustainability Due Diligence Directive (CS3D) with the transposition deadline extended to 26 July 2027. The phased approach gives companies more time to prepare for the new directives.

The Omnibus Regulation brings many benefits, including 25% reduction in overall reporting requirements while maintaining the quality of disclosures. Simplification measures will provide over €6 billion in administrative relief for companies, that’s €350 million annually.

European industries competitiveness is one of the main objectives of the EU Omnibus Regulation, aligning sustainability with economic growth. The regulation will mobilize around €50 billion in additional public and private investments in sustainable initiatives. This aligns with the EU’s broader competitiveness agenda so sustainability contributes to economic prosperity.

Simplified ESG reporting standards for SMEs are also being developed, reducing the burden for smaller companies. These standards encourage SMEs to develop a structured reporting approach aligned with their business goals, improving their overall ESG performance.

Despite the benefits the Omnibus Regulation faces several challenges and environmental risks. Political opposition may roll back corporate sustainability rules, complicating the implementation of the regulation. This pushback could come from groups opposed to corporate accountability and transparency.

SMEs will struggle with ESG reporting due to limited financial resources and lack of existing data collection processes. Without clear incentives for SMEs to comply with ESG frameworks they will see reporting as additional cost rather than business opportunity, especially when considering the potential ESG risks involved.

The EU Omnibus, aimed to simplify reporting requirements for corporates, may in fact lead to greater confusion and complications. Many corporates have spent significant figures on consultants for their Double Materiality Assessments (DMAs) and Limited Assurance, as well as having undergone organisational restructures to incorporate sustainability into other departments, such as Finance and Procurement / Supply Chain.

Addressing these challenges requires targeted support and incentives to encourage compliance and participation in sustainability initiatives.

The EU Omnibus Regulation is a big step towards harmonizing and simplifying corporate sustainability reporting across the European Union. By consolidating key directives and reducing administrative burdens the regulation will create a more efficient and effective framework for sustainability. Large companies, SMEs and direct suppliers will all feel the impact of these changes, with different implications and challenges.

As companies prepare for the changes ahead it’s important to acknowledge the benefits and address the challenges. By embracing the Omnibus Regulation companies can improve their sustainability practices, contribute to broader environmental and social goals and drive economic growth. The journey to sustainability is complex but with the right approach it can lead to a more sustainable and prosperous future.

The period for periodic assessments and updates of the due diligence policies will be extended from 1 year to 5 years. This will simplify compliance while still allowing for monitoring of due diligence.

The proposal removes the cap on pecuniary penalties, giving supervisory authorities more discretion to impose penalties. This will increase accountability and compliance within the Member States.

The CSRD will have a new application date of 2028. This is a big shift in the timeline for the sustainability reporting requirements.

The proposed amendments would raise the thresholds for the Corporate Sustainability Reporting Directive (CSRD) to apply to EU large undertakings with over 1,000 employees and specific financial metrics, ensuring greater alignment with the Corporate Sustainability Due Diligence Directive (CS3D).

The intended outcome of the proposed amendments by the European Commission is to achieve significant simplification in sustainable finance reporting, sustainability due diligence, and taxonomy. This will streamline processes and enhance clarity in these areas.